13 Questions a Financial Plan Can Help You Answer (Updated July 2023)

College Planning Investing Retirement Funding Insights13 Questions a Financial Plan Can Help You Answer

Topics: Financial Planning, Goals, Taxes, Life Insurance, Asset Allocation

Do you need a Financial Plan? As income and expenses continue to creep higher, the potential for costly mistakes becomes greater. The tax implications become more significant. Quite frankly, there’s more at risk. But a comprehensive Financial Plan can address any concerns and answer your questions about your financial future - and ultimately set your mind at ease.

Below we outline 13 questions you should ask yourself about your financial future. If you don’t know the answers, then I think it’s worth some of your effort and my time to generate a Financial Plan for you. You can start with your own Right Capital login.

A comprehensive Financial Plan can take a snapshot of where your wealth is today, help outline your goals for the future, assist you in optimizing things like taxes, life insurance and social security on your path toward or during Retirement. It can provide the probability of achieving those goals based on your current and expected income, expenses, and savings. Our Financial Planning software from Right Capital uses a simulation to generate different scenarios and stress tests and can illustrate any Estate Planning deficiencies.

13 Questions you need to ask yourself:

- What is my Net Worth?

- What are my Financial Goals?

- Can I retire when I want to?

- How much can I spend in Retirement?

- What are the most effective ways to save for Retirement?

- How can I lower my taxes?

- What is the best way to manage my debt?

- Is my college funding plan on track?

- How do I react to market fluctuations?

- What is the appropriate asset allocation right now? As I get closer to Retirement?

- Is my life insurance adequate?

- When is the optimal time to start social security?

- Will I be able to leave money to my family?

Before we get into the details:

- Our Personal Services are designed to help you establish goals and understand the probability of achieving those goals. We can manage the multiple household accounts within your portfolio to work toward those goals.

- If you’re curious about your net worth, ready to start your Financial Plan or outsource your Household CFO duties, start here by creating your own Right Capital login.

- If you’re focused on cost cutting and budgeting, check out this post: How Do I Get Out of Credit Card Debt and Start a Budget? You can also sign up for Free expense tracking.

- If you have other needs or questions about your finances, please email me: matt@mhb-advisory.com.

On a personal note

I’ve mentioned my excel spreadsheet in previous posts, and while I still appreciate its usefulness (and outlook for the next 30 years – ha!), it pales in comparison to the capabilities of the Right Capital Financial Planning software we use. I continue to refine my own personal finances using this same software that I have for clients, not just because I enjoy it, but more so because I want to make sure I give my clients all the benefit and information they need. The software can perform a variety of functions (all of which can be included in a Financial Plan), from the most basic expense tracking, up to investment analysis and probability of meeting your Retirement goals. That being said, I feel good about the answers I get for myself when I ask these 13 questions. I hope you might let me help find your answers as well. Sign up now for your Right Capital login to get started on your Financial Plan.

Let’s dive into these 13 questions:

What is my Net Worth?

Admittedly, you don’t need a Financial Plan to answer this question. Add up your assets and subtract all your liabilities and there you have it. However, our Financial Planning software makes this exercise completely brainless, prominently displaying your Net Worth on your dashboard (and updates it upon login if you link your accounts). If you haven’t really thought about it, your Net Worth is a great starting point to know where you are before you can move forward. What should your Net Worth be?

The formula for expected net worth: (Your Age) divided by (10) times (Your Pre-Tax Income)

So a 40 year-old with household income of $125,000 a year: 40 / 10 X 125,000 = $500,000.

If you do the math and you’re falling below expectations, we need to get started on your Financial Plan. Of course, if your liabilities exceed your assets, we need to have a different conversation.

What are my Financial Goals?

I’m sure we’ve all read enough quotes about the importance of goals and simply establishing goals sets you on a path to achievement. Have you thought about your Financial Goals? Do you want to buy a vacation house? Or achieve Financial Independence as quickly as possible? Or start a business? Or leave a legacy? Are these goals written down? A Financial Plan can help quantify these goals and the likelihood of achieving them.

Can I retire when I want to?

I’ve written quite a lot about retirement (or rather Financial Independence). While some are waiting to get to age 65 (or older), others seem willing to sacrifice any comfort of lifestyle to try to become Financially Independent as soon as possible. I appreciate both as I look for a good work-life balance and a suitable quality of life while loving the work that I’m doing. A Financial Plan will help you understand if you are tracking toward the age you would like to retire, and what changes to make if not.

How much can I spend in Retirement?

A rule of thumb is that what you spend now is about what you spend in retirement. Perhaps eliminating a mortgage and not saving for retirement would be offset by globetrotting and grandkids – and ultimately healthcare. I wrote a blog post that suggests unless you can live on about $40,000 a year, $1 million is not enough (according to the 4% Rule that states you can withdraw 4% of your portfolio every year in retirement). Right Capital can both generate a budget of what you spend today, plus estimate the probability of being able to spend what you want in Retirement or adjust to fit your other Financial Goals.

What are the most effective ways to save for Retirement?

Given the types of accounts you might have (401K, Roth or Traditional IRA, Taxable, etc.), what are the best options, contribution limits, tax implications of your multiple savings vehicles? How do you manage them together right now? Furthermore, how do you strategically withdraw funds from these accounts and balance with other income (pension, social security, real estate, etc.) in retirement? Since these are all questions specific to the individual, your specific Financial Plan within Right Capital can illustrate the best way to save and receive distributions over your lifetime.

How can I lower my taxes?

We all need to be mindful of tax planning – and not just on April 15th. Decisions you make year-round can affect your taxes. Can you save more in a 401K or HSA to reduce your current taxable income? Or is it better to pay more in taxes now for a future benefit by converting a traditional IRA to a Roth? A comprehensive Financial Plan can address these issues and help you understand the impact of taxes throughout your investing timeline.

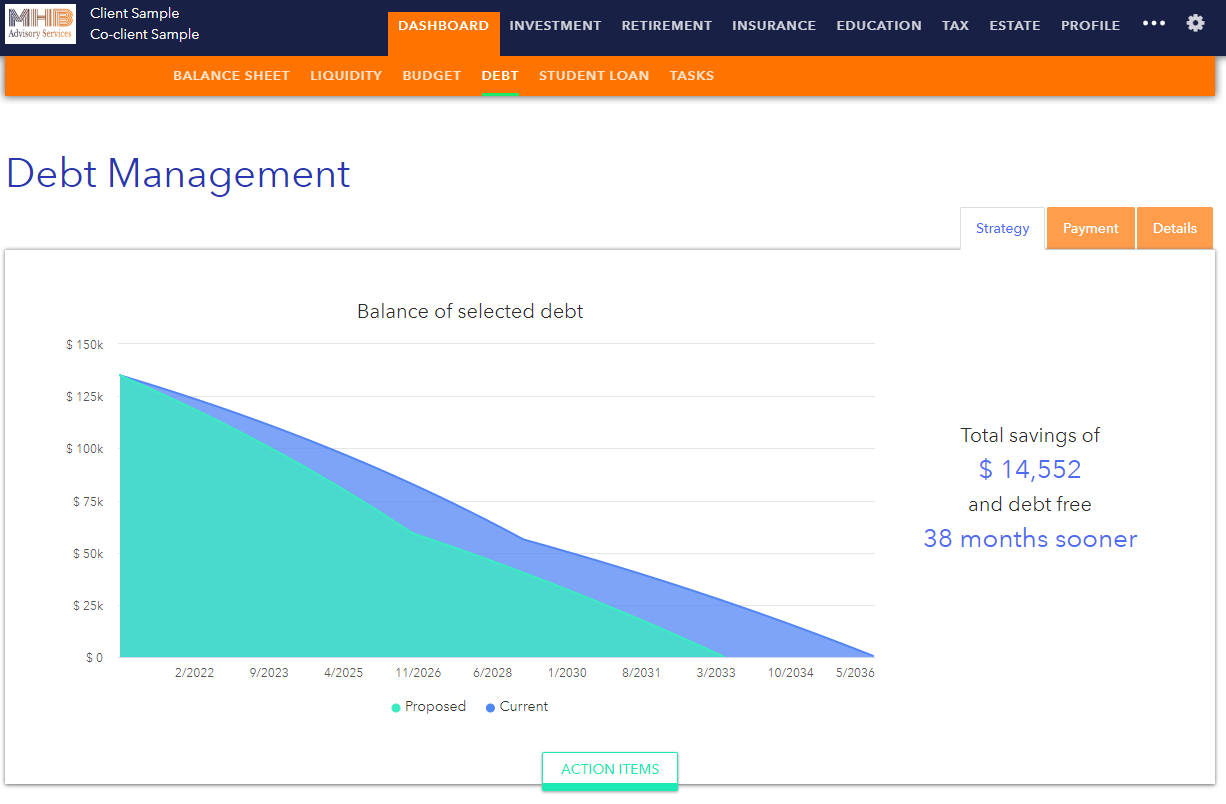

What is the best way to manage my debt?

Should you pay off your debt? Should you sacrifice savings to accelerate debt reduction? There are multiple factors here including your interest rate. Is it your primary mortgage? Or credit cards? Student Loans? A Financial Plan can evaluate these specific questions on an individual basis, largely as it relates to your comfort level with debt (risk), time horizon (are you nearing retirement?) and other factors.

Is my college funding plan on track?

Depending on your strategy for helping kids through college, you may have a 529 or other plan set up. The Right Capital Financial Planning tool can analyze holdings and determine if you are on track to meet obligations based on how much you saved, rates of return and inflation, how long until the child attends college and how much is being saved every month. The analysis can show the impact of setting aside additional funds every month as well, if for instance you want to understand the amount of money needed to fully fund your child’s education.

How do I react to market fluctuations?

Do you have a tendency to over-react to changes in the market? A Financial Plan can help you avoid an emotional response and knowing your target asset allocation can help you “buy low” and “sell high”.

What IS the appropriate asset allocation right now? As I get closer to Retirement?

Speaking of asset allocation, how do you know what the right asset mix is? It’s dependent on your willingness and ability to assume risk, plus your time horizon for investments and current amount of assets in your portfolio. You need an appropriate mix of US, foreign, small- and mid-cap stocks, as well as fixed income, real estate, commodities and cash. You want to avoid concentration in a single stock or even a single asset class as well. And obviously you want to take a more conservative approach as you get closer to retirement. All this needs to align with your financial goals as well, and a good Financial Plan can bring it all together.

Is my life insurance adequate?

For Gen X and Gen Y clients, this is probably becoming a more popular question – how much insurance do you need? And what kind? While I’m not an insurance agent (and won’t sell you any insurance products), but an analysis of your income and spending is included in our Financial Plan and can help determine your appropriate insurance coverage.

When is the optimal time to start social security?

For those closer to retirement, a more popular question is when to take social security payments. There is a substantial difference between receiving benefits as early as possible (at age 62) and deferring until age 70. If both spouses are eligible, that can change the formula as well, and our Financial Planning tool can run scenarios to show you the value of deferring social security over your lifetime.

Will I be able to leave money to my family?

For some, leaving a legacy is important, or perhaps helping the next generation (or two) while still living is important. If that is a goal, a Financial Plan can help you understand the value of that decision and the feasibility of it, all while ensuring you are able to live the life you desire in retirement.

So in closing, there are many questions you probably don’t have the answer to in terms of your financial future, but a well thought-out Financial Plan can address most of them both now and in the future. Let’s get started on your Financial Plan today.

Please check out more popular/related blog posts:

Why Should I Use a Financial Advisor for Asset Management?

How Do I Get Out of Credit Card Debt and Start a Budget?

How Can Effective Asset Management Help Me Reach Financial Independence?

How Much Money Do I Need to Save for Retirement?

How Much Should I Save for College?

Best (Most Read) MHB Advisory Blogs of 2019!

As well as other more recent posts:

Why Should Independent Contractors Use a Solo 401K for Asset Management?

10 Reasons Why You Don’t Need A Financial Advisor for Asset Management

Save, Spend or Borrow? Optimizing Asset Management for Interest Rates

4 Reasons Target Date Retirement Funds Miss the Mark for Asset Management

7 Ways to Rank Retirement Plan Options for Independent Contractors and the Self-Employed

If you or someone you know has any financial-related questions, I would love to have a conversation, so please feel free to reach out: matt@mhb-advisory.com.

And stay tuned for additional blog posts on retirement savings and other topics.

Best wishes on your financial path!

Matt

This post was created by Matt Beeby, the Founder of MHB Advisory Services. Matt has been working in Financial Services and investing in real estate since 2005, though his investment experience spans nearly two decades. He is a Christ follower, active in both his church and his neighborhood association. Matt enjoys sports and family time. Read more about Matt on his website bio.

- Disclosures:

- Information contained in this document is for informational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any product or security.

- This information is believed to be accurate and should not be considered tax or legal advice.

- Please consult tax or legal professionals for such advice and be sure to consult with a qualified financial advisor and/or tax professional before implementing any strategy discussed.

- Investments involve risk and are not guaranteed to appreciate, and past performance is not indicative of future results.

- Additional information including our privacy policy and Form ADV are available on request or can be found on our website: mhb-advisory.com.

Sources:

Photos: https://unsplash.com